Are you sitting on the fence, waiting for mortgage rates to drop just a fraction or hoping for a market crash to snag your dream home at a bargain? As a realtor in Portland, Oregon, I see this mindset all the time, and I’m here to tell you why it might not be the smartest move. In this post, I’ll break down how much you can actually save with a half-percentage-point drop in mortgage rates, share tips on saving money even with higher rates, and explain why now—fall of 2025—might be the golden opportunity for first-time buyers and current homeowners looking to upsize.

The Cost of Waiting for a Mortgage Rate Drop

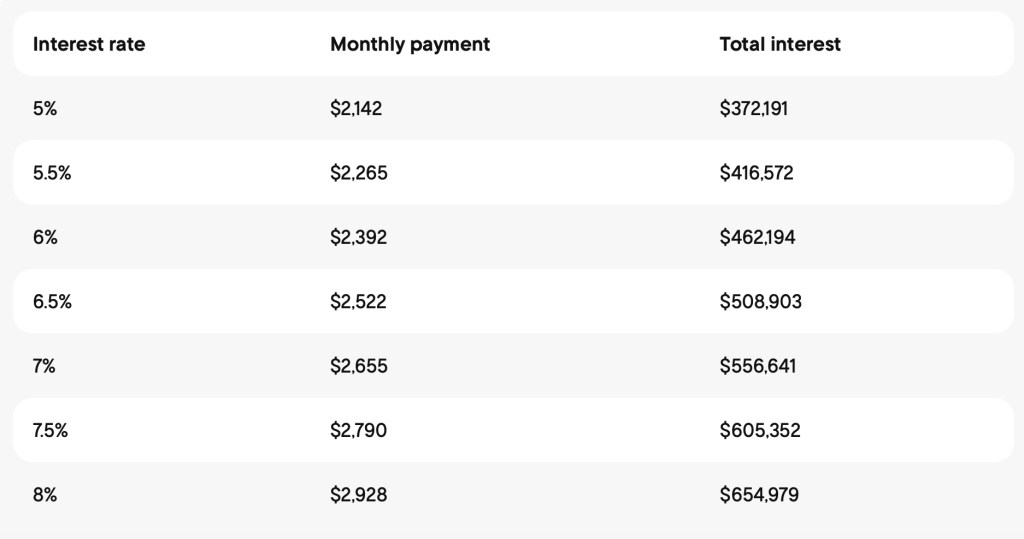

Let’s talk numbers. Many homebuyers are holding out for a mortgage rate of 5.5% or even 5%, thinking it’ll make a huge difference. But let’s put that into perspective with a $420,000 home and a 5% down payment ($21,000):

- At a 6% interest rate, your monthly payment (principal and interest) would be $2,392. Over the life of a 30-year loan, you’d pay about $462,000 in interest.

- At a 5.5% interest rate, the monthly payment drops to $2,265—a savings of $127 per month.

That’s it. Just $127 a month. Sure, saving $100 or so is nice, but is it worth waiting years for? If you’re renting and paying, say, $2,500 a month, you’re spending $60,000 over two years ($2,500 × 12 months × 2 years). That’s nearly 15% of the home’s price—enough for a solid down payment! Meanwhile, home prices in a softening market like Portland’s are negotiable, and sellers are more willing to offer credits or concessions. Waiting for a slight rate drop could mean missing out on a great deal now.

And what about those hoping for a 2008-style market crash? Good luck. The reality is, no one can predict when or if a crash will happen. Waiting for the “perfect” moment could mean missing out on today’s opportunities.

Why Now Is a Great Time to Buy

The fall of 2025 is shaping up to be a buyer’s market, especially for first-time homebuyers. Here’s why:

- Softening Market: Home prices are stabilizing or even coming down in some areas, giving buyers more negotiating power.

- Motivated Sellers: With fewer buyers in the market, sellers are more open to concessions, like covering closing costs or helping buy down your interest rate.

- More Inventory: Less demand means more homes to choose from, increasing your chances of finding the right property.

Instead of waiting for rates to drop a fraction, you can negotiate a lower purchase price or ask for seller credits to offset costs. These savings can often outweigh the benefit of a slightly lower rate.

How to Save Money at Higher Interest Rates

Even if rates are hovering around 6%, there are ways to save money and reduce your interest payments over time. Here are two strategies:

- Pay Extra Toward Principal: Adding even $50 or $100 a month to your mortgage payment can significantly reduce the interest you pay over the life of the loan. For example, paying an extra $500 a month on a $420,000 loan at 6% could shorten a 30-year mortgage to 17 years and 3 months, saving you $120,000 in interest.

- Switch to Bi-Weekly Payments: By paying half your monthly mortgage every two weeks, you’ll make the equivalent of 13 monthly payments a year instead of 12. This reduces the principal faster and cuts down on interest accrual. The compounding effect of bi-weekly payments can shave years off your loan term.

Why not opt for a 15-year mortgage? While it’s tempting, a 30-year mortgage offers more flexibility. If you hit a rough patch (like a slow sales month for someone like me), a lower monthly payment gives you breathing room. You can still pay extra toward the principal when you have the cash.

Upsizing? Why Now Might Be the Right Time

If you’re a homeowner who’s outgrown your current home—maybe you’ve got another kid on the way or need a home office—this market could work in your favor. Here’s why:

- Profit from Your Current Home: Even in a softer market, you’re likely to make a profit on the sale of your first home, especially if you bought it a several years ago at a good price.

- Bigger Savings on Bigger Homes: A softening market means you can negotiate a better deal on a larger property. Saving 5% on a $600,000 home is a lot more impactful than saving 5% on a $400,000 home. Just keep in mind, in general, higher the price range, bigger the price negotiation range.

The challenge? Timing the sale of your current home and the purchase of your new one. You’ll need to research your target neighborhood, school district, and home layout in advance. Visit two to three homes a week to get a feel for the market. And work with a sharp realtor who can coordinate the sale and purchase seamlessly—you need some luck too, but trust me, it’s a skill!

Don’t Be a Sheep Following the Herd

Too many buyers are acting like sheep, following national news headlines that scream “market crash” or “wait for lower rates.” The truth? Nobody knows when the market will hit bottom, and waiting could cost you tens of thousands in rent or missed opportunities. If you have a stable job, plan to stay in your city, and can afford a home, now is the time to act. With less competition, more inventory, and motivated sellers, the stars are aligned for buyers in fall and winter of 2025.

Final Thoughts

Don’t let a half-percentage-point difference in mortgage rates or dreams of a market crash keep you on the sidelines. The savings from a slightly lower rate are minimal compared to the benefits of buying in a buyer-friendly market. Plus, with strategies like extra principal payments or bi-weekly mortgages, you can save big even at higher rates. For those looking to upsize, a softer market means bigger savings on your next home.

If you’re in the Portland, Oregon, area and want to talk about your homebuying or selling plans, I’d love to help. You can reach me at 503-515-4499 or check the link below for a consultation. Stop sitting on the fence—fall 2025 could be your golden opportunity to own your dream home.

What do you think? Are you waiting for rates to drop, or are you ready to make a move? Share your thoughts in the comments below!

Discover more from Shawn Realty - Portland Real Estate

Subscribe to get the latest posts sent to your email.